Mobile home refinance: 2022 Loan options and requirements

Mobile home refinance guide

If you own a mobile home or manufactured home, you probably already know that mortgage rules are different for these kinds of properties.

Some mobile homes can be financed and refinanced while others can’t. Your loan options depend on when the home was built, how big it is, whether it’s fixed to its foundation, and more.

If you can refinance your mobile home or manufactured home, you might stand to save big on your monthly payments. Here’s what you should know.

In this article (Skip to…)

A note on terminology: Today’s “mobile homes” are really manufactured homes. This is true for any mobile/manufactured home built after June 15, 1976. The terms “mobile home” and “manufactured home” are often used interchangeably when referring to today’s manufactured home financing. We use both terms in this article.

Mobile home refinance requirements

Want to refinance your mobile home into a mortgage loan? If so, most lenders will require that your home be:

- On land that you own (and not located in a mobile home park)

- Affixed to a permanent foundation that conforms to HUD standards

- Titled as real property (real estate)

- Built after June 15, 1976

- Without axles, wheels, or a towing hitch

- At least 400 square feet in size

Your mobile home must also comply with building standards set by the U.S. Department of Housing and Urban Development (HUD).

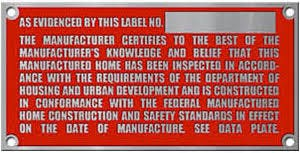

The home should have a HUD tag, which is a metal plate certification label found outside the home (pictured below). It should also have a data plate, which is a paper label found inside the home.

A mobile or manufactured home cannot be financed or refinanced without this HUD Label, which should be found on the outside of the home.

Mobile home refinance options

Eligible mobile homes can be refinanced with a variety of home mortgage programs.

Assuming the home is permanently affixed to land you own and meets property requirements, you may be able to refinance using any of the major loan programs.

Mobile/manufactured home refinance options include:

- Conventional loans

- VA loans

- USDA loans

- FHA loans

Here’s a little more information about each loan program and how to qualify.

1. Conventional loans

Backed by Fannie Mae and Freddie Mac, conventional loans are best for borrowers with at least a 620 credit score.

Homeowners typically need at least 5% equity in the home for a conventional refinance.

Fixed-rate mortgages and adjustable-rate mortgages are both available, as well as cash-out and limited cash-out refinancing in some cases. Loan terms may be as long as 30 years.

2. VA loans

VA loans are backed by the U.S. Department of Veterans Affairs and offer ultra-low interest rates for Veterans and service members.

To qualify for a VA manufactured home loan, you typically need a credit score of 620 or higher, and there’s a maximum loan term of 25 years.

3. USDA loans

Mobile/manufactured homes may be eligible for financing with a USDA loan.

These loans are backed by the U.S. Department of Agriculture and are meant to promote homeownership in under-developed regions. USDA loans are only available in designated rural areas and the mobile home must be less than one year old.

4. FHA loans

Manufactured homes that meet HUD guidelines can be refinanced via the FHA loan program.

FHA loans are guaranteed by the Federal Housing Administration and offer flexible guidelines and low down payment options for both repeat and first-time home buyers alike.

The program requires a credit score of 580 or higher and allows loan terms of up to 20-25 years for mobile/manufactured homes.

FHA Title 1 loans for mobile homes

If you rent the land your mobile home is on, you’re still in luck. You may qualify for an FHA Title 1 mortgage loan.

To qualify, you must:

- Lease your lot from an FHA-compliant community or site

- Have an FHA-eligible lease in effect

- Live in the mobile home as your primary residence

- Have your mobile home set on a permanent foundation

Keep in mind that many landlords and mobile home communities don’t comply with FHA mortgage standards. Also, it may be difficult to find a Title 1 mortgage lender.

Steps to getting a manufactured or mobile home refinance

Who refinances mobile homes?

Not all lenders offer manufactured or mobile home loans. So even if your property meets guidelines for mortgage financing, you may need to do some digging to find a lender that will work with you.

One good option could be to contact a mortgage broker to help with your search.

Brokers work with multiple mortgage lenders and may be able to direct you toward a lender that offers manufactured home refinancing in your area.

Also note that mortgage lenders enforce minimum loan amounts, which could potentially restrict financing options for lower-priced mobile/manufactured homes.

Converting your mobile home to real property

One of the biggest steps involved with mobile home refinancing is converting your personal property title to a real estate title.

To be eligible for a mobile/manufactured home loan, your home needs to be considered “real property” rather than personal property.

Mobile or manufactured homes that don’t meet the requirements listed above are considered personal property. So you might need to make some changes to the home before you can be eligible for a mortgage refinance.

Converting your mobile home title into real property requires:

- Certificate of title to your mobile home

- Copy of your mobile home’s certificate of origin

- Deed to the land on which your mobile home’s permanent foundation is fixed

This process is easier today in some states, including Virginia, Maryland, Tennessee, Nebraska, Illinois, Missouri, Alaska, Iowa, and North Dakota.

“In addition, you’ll need a foundation certification performed by a licensed structural engineer,” explains Raymond Brousseau, Partner with River City Mortgage.

“Plus, the home needs sufficient homeowners insurance coverage to qualify for a mortgage loan,” he adds.

Mobile, manufactured, modular home? It makes a difference for refinancing

Today, mobile homes are more often called manufactured homes or modular homes. In fact, the terms are interchangeable in the industry. But there are slight differences — and they can affect financing and refinancing options for your mobile home.

Brousseau explains:

- A mobile home is a residence that has or used to have axles and wheels. It’s titled as a motor vehicle. “True” mobile homes were built prior to June 15, 1976

- A manufactured home is constructed entirely in a factory. It’s brought to the home site in one or more pieces. These come in both single-wide and double-wide varieties

- A modular home is mostly constructed in a factory, but it’s brought to the home site in multiple pieces to finish construction. Once built, you can’t move a modular home. These also come in both single-wide and double-wide homes

If your home is still technically “mobile,” it cannot be financed or refinanced with a mortgage loan. But if it’s fixed toa foundation and considered “real property,” it can likely be financed or refinanced.

If your home is fixed to its foundation and considered “real property,” it can likely be financed or refinanced with a mortgage loan.

Technically, any manufactured home built prior to June 15, 1976 is considered a bona fide “mobile home.” And those built after that date are considered manufactured homes.

Many mobile homes are permanently affixed to a foundation. These are much easier to refinance if you qualify. That’s because they’re titled as “real property.”

But mobile homes not permanently affixed to a foundation are usually titled and financed as “personal property.”

Mortgages vs. personal property loans: What’s best for a mobile home refinance loan?

If your manufactured home is titled as real property, you may currently have a mortgage loan.

If your manufactured home is titled as personal property, however, you likely have a personal property loan. These are also called “chattel loans” — and they often come with higher interest rates than mortgage loans.

The Consumer Financial Protection Bureau reported that, a few years ago, around two in three purchase loans for mobile homes were higher-priced than mortgage loans. Many of these are chattel loans.

“If you rent the site your mobile home is on, often the only financing option is a personal property loan,” Brousseau says.

“If you currently have a personal property loan, you’ll have to convert the title and the loan to a mortgage loan, if possible, in order to refinance at today’s mortgage rates.”

The good news? If you meet the requirements, you can refinance either type of loan and likely take advantage of today’s lower interest rates.

However, if you currently have a personal property loan, you’ll want to convert the title and the loan to a mortgage loan if possible.

That way you can refinance into today’s mortgage rates — which are likely to be much lower than your current personal property loan rate.

That requires owning the land you’re on and setting the home permanently on a foundation.

Is refinancing a mobile home worth it?

Today’s mortgage rates are still relatively low. Many homeowners who bought a few years ago could lower their interest rate and mortgage payments by refinancing in this environment.

That might be especially true for mobile and manufactured homeowners.

Chattel loans have interest rates typically over 7 percent. Refinance to a mortgage loan, and you may get a rate closer to 3% according to the most recent Freddie Mac data.

That can save thousands over the life of the loan. Plus, if you pay private mortgage insurance (PMI), you could refinance and eliminate that if you’ve earned enough equity in your mobile home.

Drawbacks to refinancing a mobile home

Qualifying for a mobile home refinance can be costly, Brousseau cautions. Some of the disadvantages of obtaining a mobile home refinance loan include:

- There are refinance closing costs to consider, and homeowners who need to convert a personal property title to a real property title will face additional upfront fees

- You may need to hire a real estate lawyer or title company for help with this process

- You may pay more in real estate taxes after converting your title than you would have paid for property taxes

- Setting your mobile home on a permanent foundation can set you back a few thousand dollars

For more information, talk to a mortgage lender or broker who can walk you through your mobile home refinance options and discuss eligibility.

Today’s mobile home refinance rates

Crunch the numbers. And determine how much longer you’ll stay in your mobile home.

Provided you qualify for a lower interest rate, there’s a good chance you could save by refinancing your mobile or manufactured home — even when the upfront costs are considered.

Not sure whether you’d qualify? You can contact a mortgage lender to check your mobile home refinance eligibility.

Loan officers are able to look at your unique situation to tell you whether you’re eligible to refinance and how much you might save.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Comments are closed.