How much should you put down on a house? Not 20%

How much should you put down on a house?

First things first: The idea that you have to put 20% down on a house is a myth.

The average first–time home buyer puts just 6% down, and certain loan programs allow as little as 3% or even zero down.

You shouldn’t think it’s conservative to make a large down payment on a home, or risky to make a small down payment. The right amount depends on your current savings and your home buying goals.

If you can buy a house with less money down and become a homeowner sooner, that’s often the right choice.

Verify your low-down-payment loan eligibility. Start here (Feb 5th, 2022)

In this article (Skip to…)

>Related: How to buy a house with $0 down: First–time home buyer

What is a down payment?

In real estate, a down payment is the amount of cash you put upfront towards the purchase of a home.

Down payments vary in size and are typically expressed as a percentage.

For example, if you’re buying a home for $400,000 and bring $80,000 toward the purchase, your down payment is 20%.

Similarly, if you brought $12,000 cash to your closing, your down payment would be 3%.

The term “down payment” exists because very few people opt to pay for homes using cash.

How much is the down payment on a house?

How much down payment you need for a house depends on which type of mortgage you get.

- A conventional loan is the most popular loan option

- Conventional down payment requirements start at 3–5% down

- On a $250,000 house, that’s a $7,500–$12,500 down payment

However, you would need 20% down to avoid private mortgage insurance (PMI) on a conventional mortgage. Many buyers want to avoid PMI because it increases your monthly mortgage payment. Twenty percent down comes out to $50,000 on a $250,000 home.

PMI rules are not set in stone, though.

“Some states have their own rules about PMI,” says Jon Meyer, The Mortgage Reports loan expert and licensed MLO. “As an example, in California, it’s possible to not have private mortgage insurance when a borrower has a higher loan–to–value ratio.”

Another low–down–payment option is the FHA mortgage program.

- FHA loans let you buy with 3.5% down

- That would be $8,750 on a $250,000 house

Some loan types will even let you buy with zero down. These include two government–backed programs:

- VA loans allow 0% down

- USDA loans allow 0% down

However, you’ll likely still have to cover some or all of your upfront closing costs with cash. So even with a zero–down program, you’ll likely need to bring some money to the closing table.

Verify your low-down-payment loan eligibility. Start here (Feb 5th, 2022)

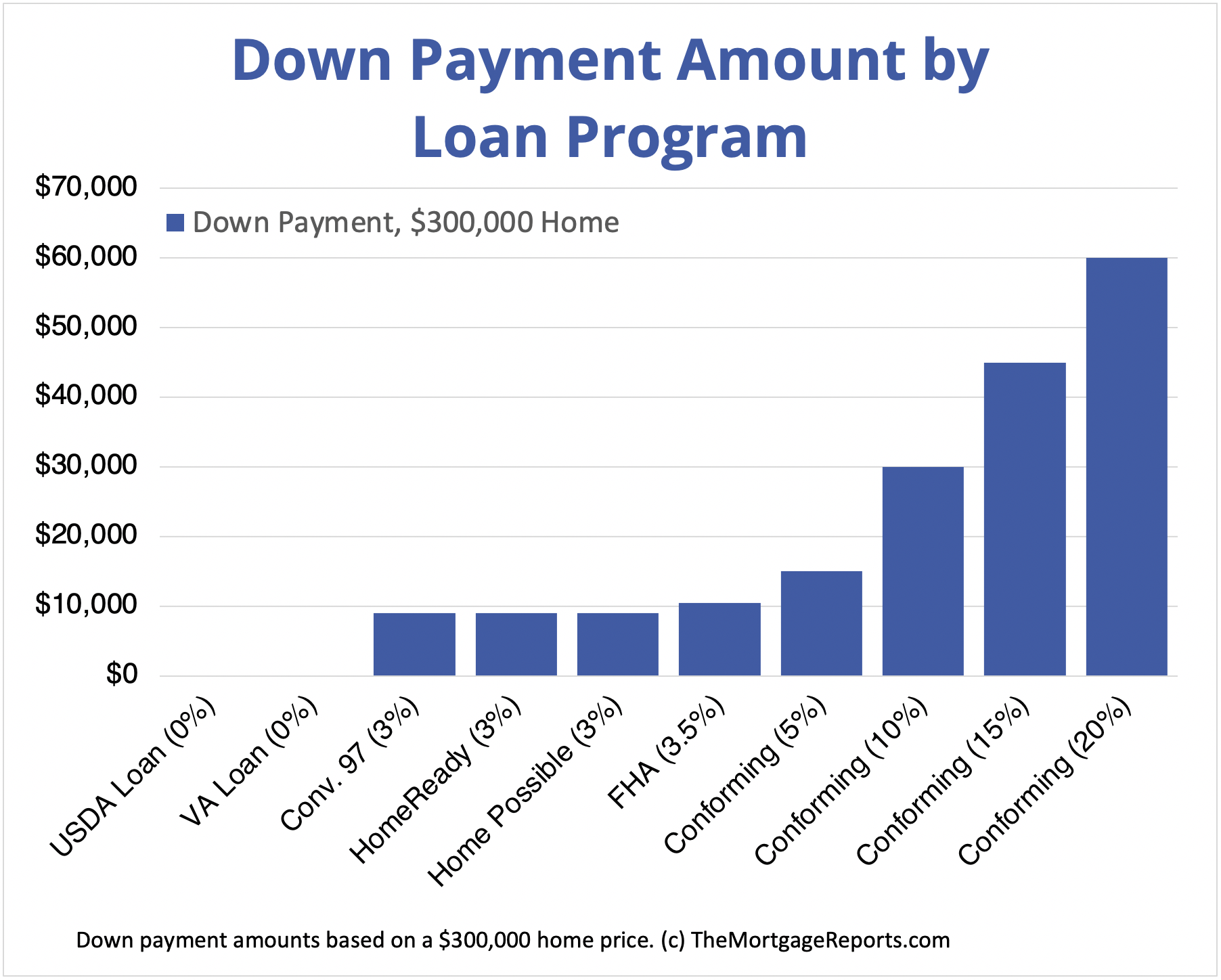

Down payment requirements for mortgage loans

Depending on the mortgage program for which you’re applying, there’s going to be a specified minimum down payment amount.

For today’s most widely–used mortgage programs, down payment requirements are:

- Conventional Loan (with PMI): 3% minimum

- Conventional Loan (without PMI): 20% minimum

- FHA Loans are guaranteed by the Federal Housing Administration and require as little as 3.5% down

- VA Loans are backed by the Department of Veterans Affairs and have no down payment requirements. VA loans are designed for active military, veterans, and some surviving spouses

- USDA Loans are guaranteed by the U.S. Department of Agriculture and require nothing down. However, USDA loans are devised for home buyers in suburban and rural areas who meet income limits and other eligibility criteria

- Fannie Mae HomeReady Loan: 3% down minimum

- Freddie Mac Home Possible: 3% down minimum

- Jumbo Loan: typically 10% down, depending on lender

These requirements may also vary by lender and a home buyer’s financial situation.

For example, an FHA loan requires only 3.5% down with a credit score of 580 or more, but that requirement changes to 10% down for borrowers with credit scores between 500–579.

Remember, though, that these requirements are just the minimum. As a mortgage borrower, it’s your right to put down as much on a home as you like. Ans in some cases, it can make sense to put down more than the minimum requirement.

That begs the question: How much money should you put down?

How much should you put down on a house?

Should you put 20% down on a house, even though it’s not required? In many cases, the answer is no.

In fact, most people put only 6–12% down. But the right amount depends on your financial situation.

For instance: If you have significant cash reserves in your savings account, but relatively low income, making the biggest down payment possible can be a good idea. That’s because a large down payment shrinks your loan amount and reduces your monthly mortgage payment.

Or maybe your situation is reversed.

Maybe you may have a good household income but no emergency fund or little savings in the bank. In this instance, it may be best to use a low– or no–down–payment loan, while planning to cancel your mortgage insurance at some point in the future.

There are other scenarios where it makes sense to put more down, too.

For instance, if you’re buying a condo:

- Condo mortgage rates are approximately 12.5 basis points (0.125%) lower for loans where the loan–to–value ratio (LTV) is 75% or less.

- Putting 25% down on a condo, therefore, gets you access to lower interest rates. So if you’re putting down 20%, consider an additional 5%, and you’ll likely get a lower mortgage rate

Making a larger down payment can shrink your costs with FHA loans, too.

Under the new FHA mortgage insurance rules, when you use a 30–year fixed rate FHA mortgage and make a down payment of 3.5 percent, your FHA mortgage insurance premium (MIP) is 0.85% annually.

However, when you increase your down payment to 5%, FHA MIP drops to 0.80%. This could save you money each month and over the life of the loan.

At the end of the day, the “right” down payment depends on your personal finances and the home you plan to buy.

Check your down payment options. Start here (Feb 5th, 2022)

Benefits of a 20% down payment

A large down payment helps you afford more house with the same monthly income.

Say a buyer wants to spend $1,000 per month for principal, interest, and mortgage insurance (when required). Making a 20% down payment instead of a 3% raises their home buying budget by over $100,000 – all while maintaining the same monthly payment.

Here’s how much house the home buyer in this example can purchase at a 4% mortgage rate. The home price varies with the amount the buyer puts down.

| Down Payment (%) | Down Payment ($) | Monthly Payment (Principal & Interest / PMI) | Home Price You Can Afford |

| 3% | $884 / $116 | $154,500 | |

| 5% | $8,780 | $896 / $104 | $175,500 |

| 10% | $91,310 | $913 / $87 | $193,000 |

| 20% | $52,370 | $1,000 / $0 | $261,500 |

Even though a bigger down payment can help you afford a larger home loan, by no means should home buyers tap their emergency funds to stretch their down payment level.

Disadvantages of putting 20% down

As a homeowner, it’s likely your home will be your biggest asset. The property may even be worth more than all your other investments combined.

In this way, your home is both a shelter and an investment. And once we view our home as an investment, it can guide the decisions we make about our money.

The riskiest decision someone can make when purchasing a new home? Making too big of a down payment.

A big down payment will lower your rate of return

The first reason why conservative investors should monitor their down payment size is that it will limit your home’s return on investment.

Consider a home that appreciates at the long–time national average of near 5%.

Today, your home is worth $400,000. In a year, it’s worth $420,000. Regardless of your down payment, the home is worth $20,000 more.

That down payment will affect your rate of return.

- With 20% down on the home – $80,000 – your rate of return is 25%

- With 3% down on the home – $12,000 – your rate of return is 167%

That’s a huge difference.

We must also consider the higher mortgage rate plus mandatory private mortgage insurance which accompanies a conventional 3%–down loan. Low–down–payment loans can cost more each month.

Assuming a 175 basis point (1.75%) bump from rate and PMI combined, we find that a low–down–payment homeowner pays an extra $6,780 per year to live in their home.

With 3% down, and making an adjustment for rate and PMI, the rate of return on a low–down–payment loan is still 105%.

The less you put down, the larger your potential return on investment.

Check your eligibility for a low down payment loan. Start here (Feb 5th, 2022)

Once you make your down payment, you can’t get the money back easily

There are other down payment considerations, too.

Once you make a down payment, you can’t access that money unless you sell the house or take out a loan against it.

This is because, at the time of purchase, whatever down payment you make on the home gets converted immediately from cash into a different type of asset known as home equity.

Home equity is the monetary difference between what your home is worth on paper, and what you owe to your mortgage provider.

Unlike cash, home equity is an illiquid asset, which means that it can’t be readily accessed or spent.

All things equal, it’s better to hold liquid assets as an investor, rather than illiquid assets. In case of an emergency, you can use your liquid assets to relieve some of the pressure.

It’s among the reasons why conservative investors prefer making as small of a down payment as possible.

When you make a small down payment, you keep cash in your savings account rather than tying it up in real estate.

It’s nice to make a large down payment because it lowers the total cost of your monthly payment – you can see that on a mortgage calculator. But when you make a large down payment at the expense of your own liquidity, you may put yourself at risk.

You’re at risk when your home value drops

A third reason to consider a smaller down payment is the link between the economy and U.S. home prices.

In general, as the U.S. economy grows, home values rise. And, conversely, when the U.S. economy sags, home values sink.

Because of this link between the economy and home values, buyers who make a large down payment find themselves over–exposed to an economic downturn, as compared to buyers whose down payments are small.

“However, an exception is when you’re refinancing your home. If home prices fall and you have less equity, then you will be less likely to refinance,” says Meyer.

Big vs. small down payment example

We can use a real–world example from the last decade’s housing market downturn to highlight this type of connection.

Consider the purchase of a $400,000 home and two home buyers, each with different ideas about how to buy a home.

- One buyer puts 20% down to avoid paying private mortgage insurance

- Another buyer wants to stay as liquid as possible, choosing to use the FHA mortgage program, which allows for a down payment of just 3.5%

At the time of purchase, the first buyer takes $80,000 from the bank and converts it to illiquid home equity. The second buyer, using an FHA mortgage, puts $14,000 into the home.

- Over the next two years, the economy takes a turn for the worse. Home values sink and, in some markets, values drop as much as 20%.

- Both buyers’ homes are now worth $320,000, and neither homeowner has built home equity.

However, there’s a big difference between their financial situations.

- The first buyer – the one who made the large down payment – $80,000 has evaporated into the housing market. That money is lost and cannot be recouped except through the housing market’s recovery.

- The second buyer, though, only “lost” $14,000. Yes, the home is “underwater” at this point, with more money owed on the home than what the home is worth, but that’s a risk that’s on the bank and not the borrower.

And, in the event of default, which homeowner do you think the bank would be more likely to foreclose upon?

It’s counter–intuitive, but the buyer who made a large down payment is less likely to get relief during a time of crisis and is more likely to face eviction.

Why is this true? Because when a homeowner has at least some equity, the bank’s losses are limited when the home is sold at foreclosure. The homeowner’s 20% home equity is already gone, after all, and the remaining losses can be absorbed by the bank.

Foreclosing on an underwater home, by contrast, can lead to great losses. All of the money lost is money lent or lost by the bank.

A conservative buyer will recognize, then, that investment risk increases with the size of down payment. The smaller the down payment, the smaller the risk.

What if I can’t afford the down payment?

Not everyone qualifies for a zero–down mortgage. Most borrowers need at least 3% down for a conventional mortgage or 3.5% down for an FHA loan.

But what if you can’t quite afford the minimum down payment? Three percent down on a $300,000 home is still $9,000 – a considerable amount of money.

Luckily there are programs that can help.

For example, every state has multiple down payment assistance programs (DPAs). These programs – often funded by state and local governments and nonprofits – offer money to make homeownership more accessible for lower–income or disadvantaged home buyers.

DPA funds can come in the form of a grant or loan, and the loans are often forgiven if you live in the home for a certain period of time.

To find out whether you’re eligible for assistance, ask your Realtor or lender to help you find and apply for programs in your area.

Verify your low-down-payment loan eligibility. Start here (Feb 5th, 2022)

20% down payment FAQ

You do not have to put 20 percent down on a house. In fact, the average down payment for first–time buyers is just 6 percent. And there are loan programs that let you put as little as zero down. However, a smaller down payment means a more expensive mortgage long–term. With less than 20 percent down on a house purchase, you will have a bigger loan and higher monthly payments. You’ll likely also have to pay for mortgage insurance, which can be expensive.

The “20 percent down rule” is really a myth. Typically, mortgage lenders want you to put 20 percent down on a home purchase because it lowers their lending risk. It’s also a “rule” that most programs charge mortgage insurance if you put less than 20 percent down (though some loans avoid this). But it’s NOT a rule that you must put 20 percent down. Down payment options for major loan programs range from 0 to 3, 5, or 10 percent.

It’s not always better to make a large down payment on a house. When it comes to making a down payment, the choice should depend on your own financial goals. It’s better to put 20 percent down if you want the lowest possible interest rate and monthly payment. But if you want to get into a house now and start building equity, it may be better to buy with a smaller down payment – say 5 to 10 percent down. You might also want to make a small down payment to avoid draining your savings. Remember, you can always refinance into a lower rate with no mortgage insurance later on down the road.

It’s possible to avoid PMI with less than 20 percent down. If you want to avoid PMI, look for lender–paid mortgage insurance, a piggyback loan, or a bank with special no–PMI loans. But remember, there’s no free lunch. To avoid PMI, you’ll likely have to pay a higher interest rate. And many banks with no–PMI loans have special qualifications, like being a first–time or low–income home buyer.

The biggest benefits of putting 20 percent down on a house are having a smaller loan size, lower monthly payments, and no mortgage insurance. For example, imagine you’re buying a house worth $300,000 at a 4 percent interest rate. With 20 percent down and no mortgage insurance, your monthly principal and interest payment comes out to $1,150. With 10 percent down and mortgage insurance included, payments jump to $1,450 per month. Here, putting 20 percent down instead of 10 saves you $300 per month.

It is absolutely ok to put 10 percent down on a house. In fact, first–time buyers put down only 6 percent on average. Just note that with 10 percent down, you’ll have a higher monthly payment than if you’d put 20 percent down. For example, a $300,000 home with a 4 percent mortgage rate would cost about $1,450 per month with 10 percent down, and just $1,150 per month with 20 percent down.

The biggest drawback to putting 10 percent down is that you’ll likely have to pay mortgage insurance. Though if you use an FHA loan, a 10 percent or higher down payment shortens your mortgage insurance term to 11 years instead of the full loan term. Or you can put just 10% down and avoid mortgage insurance with a “piggyback loan,” which is a second, smaller loan that acts as part of your down payment.

What are today’s mortgage rates?

Today’s mortgage rates are still near historic lows, even for borrowers with less than 20% down. In fact, borrowers with low–down–payment government loans often get access to below–market rates.

So don’t write off home buying because you’re waiting to save 20% down. Many buyers can qualify today and don’t even know it.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Comments are closed.