Will inflation and rising rates cause a housing market crash?

Rising rates will change the housing market

With interest rates going up, will home price growth finally go down?

It’s a fair question. And while it’s something home buyers desperately hope for after what we’ve seen over the past year, the answer isn’t totally black and white.

Rising mortgage rates impact the mechanics of the entire housing market. And that should be expected in 2022 with the Federal Reserve signaling upcoming rate hikes.

But while affordability could take a hit, buying a home may be an even smarter move given how inflation will push rent prices higher.

Verify your home buying eligibility. Start here (Feb 18th, 2022)

How will home prices be affected?

To be clear, interest rates do not directly correlate with home prices, and vice versa. However, low rates stoke home buyer demand and higher demand leads to higher sales prices.

“I don’t anticipate that housing prices will come down – they just won’t continue to grow exponentially as they have in the past year.”

—Jess Kennedy, Co-founder and COO, Beeline

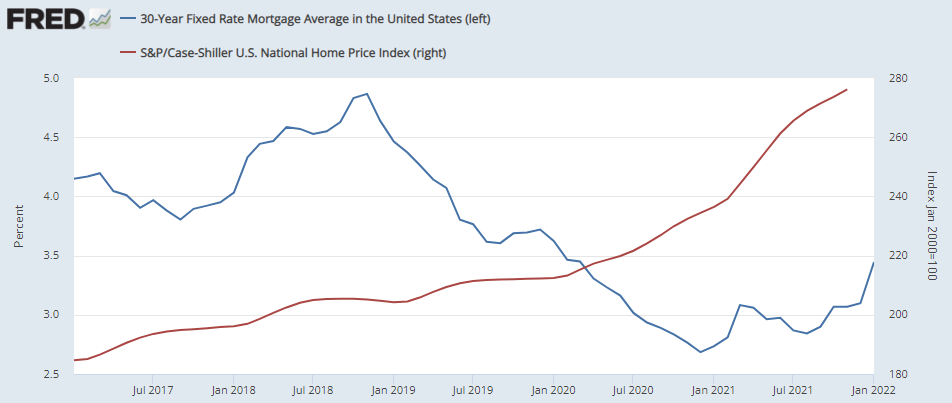

The graph below shows the relationship between monthly averages of the 30–year fixed mortgage rate and the S&P/Case–Shiller Index, which measures the change in housing values by tracking single–family home purchase prices.

Sources: Freddie Mac; S&P Dow Jones Indices LLC

While not completely mirroring each other over the past five years (and mortgage rates, by nature, are more volatile), home values took off when interest rates cratered in 2020.

A similar pattern could unfold this year with mortgage rates expected to rise further and housing prices projected to grow at a lesser pace. Although, buyers should account for the lack of inventory keeping prices inflated.

Jess Kennedy, co-founder and COO at Beeline

“When you look at where the housing market is right now, you still see big gaps between available supply and demand. Until that demand is lowered due to rising rates, housing prices won’t go down.

“As supply and demand come into line with one another (finally), we will see a normalization of the market but I don’t anticipate that housing prices will come down – they just won’t continue to grow exponentially as they have in the past year. In the short term as buyers look to find a property before higher rates impact them, we could actually see home prices driven higher.”

Where does affordability go from here?

As interest rates rise, affordability tends to decline because house hunters have less buying power.

However, affordability is relative and goes beyond just listing prices and mortgage rates. Home buying comes with additional advantages and a fixed–rate mortgage could be your best friend in the face of this year’s high inflation.

“Remember that affordability is continually a comparison of renting v.s. buying. As rent continues to increase due to inflation, homeownership may still be the cheaper alternative.”

—Ward Morrison, President and CEO, Motto Mortgage

Brandon Haefele, CEO at Catalyst Mortgage

“People normally just look at the price of a house, but they’re not counting the potential tax benefits, a fixed payment, or the appreciation of equity. You build equity with a mortgage and markets are going to continue increasing because there’s a supply and demand issue.

Plus, I think there’s one thing that as an industry and consumers across the board still are not taking into account when they are thinking about rising home prices: inflation bringing rising wages.

If you get a home and lock in a fixed–rate mortgage now, you’re hedging against any inflation that goes into 2022, 2023 and 2024, whereas inflation drives rent prices up.”

Ward Morrison, president and CEO of Motto Mortgage

“As interest rates rise, there always tends to be an inverse reaction to home valuations. When interest rates increase, affordability of home buying decreases. To offset this issue of affordability, the market stabilizes and home prices go down.

However, I don’t anticipate as big of a decline in home buying as we might normally expect because real estate supply and demand is so off balance right now that we likely won’t see prices decrease as rapidly as we have in the past.

Overall, homeownership continues to be the best savings vehicle for the average American. You must remember that affordability is continually a comparison of renting v.s. buying. As rent continues to increase due to inflation, homeownership may still be the cheaper alternative.”

Verify your home buying eligibility. Start here (Feb 18th, 2022)

Is the housing market going to crash?

With such rapid and sustained price increases throughout 2021, people wonder if another bursting housing bubble could be on the horizon.

However, parallels drawn to the 2008 mortgage crisis aren’t accurate since underwriting standards tightened significantly since then. The current period of skyrocketing housing value gains has been driven by historically low for–sale supply combined with elevated demand.

The pace of home price growth will likely slow this year but any kind of market crash scenario seems very unlikely and shouldn’t be counted on. Because of this, acting as soon as possible in your home buying or refinancing journey probably is the best way to spend less money.

With the Fed’s projected rate hikes, the window for refinancing borrowers closes quickly and will remove some potential buyers due to affordability constraints.

Ward Morrison, president and CEO of Motto Mortgage

“In the short term, increasing interest rates can be a positive thing because it may help urge sellers to move off the fence as prices potentially peak, creating more buying opportunities.

When it comes to individual segments of potential home buyers, the middle and lower end of the socioeconomic paradigm will see the most impact and inverse reaction to increasing interest rates and home prices. It will have little–to–no impact on those within the higher end of the market.”

Glen Pizzolorusso, licensed associate real estate broker at Compass

“I recommend everyone buy while rates are low and not worry about the uncertainty in home prices. Given that this is being driven by true supply and demand (not artificial demand caused by easy credit, à la 2004–2007), I do not see the market price of homes decreasing any time soon. If anything they will continue to increase with minor corrections in some isolated markets.”

Ralph McLaughlin, chief economist at Kukun

“Mortgage lenders are facing less refi interest with a rising rate environment. However, people who are staying put will still need to maintain their homes, so home equity products are likely to see much more renewed interest as those make more sense to homeowners.

This is the backdrop of what 2022 holds for housing finance: parts of it will still look like mini–versions of 2021. Rising prices? Yes, in most places, just not as crazy. Affordability will take a hit with rates, but those who can find a home and buy, they’ll get it done.

So there won’t be a large–scale collapse of the mortgage market. The one “if” (and it’s a big “if”), is if the economy, in general, can remain in positive territory. That’s tougher to call, at the moment, as there is volatility in other macroeconomic factors, primarily consumer confidence and jobs, that can throw a wrench into the recovery.”

Brandon Haefele, CEO at Catalyst Mortgage

“I think we’re now going to start seeing individual markets potentially have some slowdown. And my reasoning is we still have extremely low inventory. But it’s not going to go the other way and crash.

Nobody in history has seen mass migration to where you can work anywhere and live anywhere, as you now can in our new era. I really recommend people talk to real estate agents that live in that area.

Look at specifics, work with local lenders, local underwriters, local real estate agents, because they know the market best and they can give you a better understanding than somebody going off data from 10,000 feet.”

Your next move

The climbing interest rate environment will impact every facet of the housing market. Of course, it’s important to remember that even if rates go above 4%, they’re still low from a historical perspective.

Whether you’re looking to buy or refi, checking your mortgage eligibility and reaching out to a lender is usually the best way to get started.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Comments are closed.