Who pays closing costs? Typical costs for buyer and seller

Who pays closing costs?

Typically, buyers and sellers each pay their own closing costs.

A home buyer is likely to pay between 2% and 5% of their loan amount in closing costs, while the seller could pay 5% to 6% of the sale price to their real estate agent.

But it doesn’t always work out that way.

Buyers may be able to get someone else – like the seller, the lender, or a down payment assistance program – to cover some or all of their out–of–pocket expenses. Here’s how.

In this article (Skip to…)

Buyer closing costs

When most people think about closing costs, they’re thinking about the buyer’s closing costs. These are your out–of–pocket fees to set up a home loan, get the house appraised, have the title transferred to your name, and so on.

Buyers typically pay between 2% and 5% of their loan amount in closing costs.

That means if you’re taking out a $200,000 mortgage loan, closing costs could range from $4,000 to $10,000 (though they’d likely be on the lower end of that spectrum).

The amount a home buyer has to pay in closing costs can vary a lot depending on the home price, location, and other factors.

Typical closing costs paid by the buyer

Here are the most common and expensive closing costs home buyers have to pay:

- Origination fee: This is the lender’s charge for its services, including the cost to verify your documents, process your application, and get the loan set up. The origination fee is often around 1% of the loan amount

- Appraisal fee: A home appraisal typically costs around $500, but could be as much as $1,000. The home appraisal usually follows an inspection of the property

- Title search and title insurance: A title search makes sure your new home’s title is clear, meaning no one else can claim rights to the home or property. Title insurance provides protection against undiscovered claims

- Upfront mortgage insurance or funding fee: Some types of home loans require an upfront fee to insure or guarantee the mortgage. Government–backed loans, including FHA loans, VA loans, and USDA mortgages, all have such a fee, though you can typically roll this into your loan amount instead of paying at closing

- Discount points: Discount points let you buy a lower interest rate by paying an extra fee at closing, typically equal to 1% of the loan amount. Check your rate quotes for discount points, as some lenders offer lower mortgage rates upfront assuming the buyer will buy points at closing

- Escrow: You’ll have to pay some of your future property taxes and homeowners insurance premiums upfront. That prepaid money will be placed in an escrow account and disbursed by your as necessary

Your down payment will also be due at closing, although it’s not typically thought of as a closing cost. Yet, it may show on the disclosures as part of the cash needed to close.

Any earnest money put into escrow when you made an offer on the house will be credited toward your down payment at closing by your escrow company.

Also note that closing costs depend on the mortgage lender.

While some closing costs are set by third parties and cannot be changed, others are controlled by the lender and can vary a lot.

Common third–party closing costs for the buyer

- Credit report fee: Fee to pull your FICO credit score from the three main credit–reporting bureaus

- Attorney fees: Fee paid to a real estate attorney for reviewing home purchase agreements. Not all states require this cost

- Recording fees: Fees paid to your local government to process records when a property’s ownership changes hands

- Homeowners association transfer fees: An HOA transfer fee only applies for homes within a planned community that is governed by an HOA. Usually, the seller pays. This fee is separate from monthly HOA dues

- Home inspection: Cost of hiring a home inspector to assess the property’s condition

While the above third–party fees are not necessarily negotiable, you can save money by choosing which vendor you choose to perform services. Of course, this wouldn’t apply to your county recording fees, which are usually a set fee charged by your local government.

As a rule of thumb, shopping for the lowest fees is a simple and effective way to lower the closing costs of your home buying process.

Seller closing costs

Sellers have closing costs, too. Unfortunately, they don’t have the same flexibility to shop for and negotiate lower closing costs that buyers do.

But home sellers should still be aware and prepared to pay the out–of–pocket charges on their sale.

The biggest single item the seller pays is usually the commission paid to your real estate agent, mortgage broker, or Realtor. That’s commonly 5% or 6% of the purchase price. Yes, that’s often shared with the buyer’s agent– but it’s typically still paid for by the seller.

Home sellers should also expect charges for transfer taxes, title fees, escrow fees, and so on.

There’s not much you can do about some taxes and fees. But your real estate commission may well be negotiable.

If you’re looking to avoid closing costs as a seller, be sure to explore alternatives: Selling your home yourself; finding a discount broker, or using a different real estate agent.

Checking all your options will give you a basis for negotiation.

If you want a full service, you’re going to have to pay for it. But sellers can often shop around and get a lower commission rate than the one they were originally quoted.

Closing costs vary by loan type

For borrowers, the type of mortgage you choose can have a big effect on your closing costs. And the biggest of these is mortgage insurance.

FHA upfront mortgage insurance premium (UFMIP)

FHA loans require annual mortgage insurance and an upfront insurance fee.

The latter – called upfront mortgage insurance premium, or UFMIP – is equal to 1.75% of the loan amount, or $1,750 for every $100K borrowed.

Despite its name, FHA upfront mortgage insurance doesn’t have to be paid at closing. Most borrowers roll this cost into their loan amount rather than pay it with cash.

Rolling UFMIP into your loan will greatly reduce your closing costs. But it does mean you’ll pay interest on the fee over the life of your home loan.

Keep in mind that UFMIP is separate from an FHA loan’s ongoing mortgage insurance. It’s also entirely different from private mortgage insurance (PMI) that is paid by buyers who put less than a 20% down payment on a conventional loan.

VA loan funding fee

VA loans do not require annual mortgage insurance. But they do require a one–time ‘funding fee’ due at closing.

For first–time home buyers, the VA funding fee is usually equal to 2.3% of the loan amount. Buyers who’ve used a VA loan before will pay 3.6% of their loan amount. If you make a down payment of 5% or more, the VA funding fee is reduced.

VA home buyers also have the option to roll this fee into their loan amount instead of paying it along with their closing costs.

USDA guarantee fee

Like the FHA loan, the USDA home loan program requires both an upfront mortgage insurance fee and an annual one.

USDA’s upfront fee is equal to 1% of the loan amount and can be added to the mortgage balance to reduce closing costs.

How to shop for the lowest closing costs

The amount you pay in closing costs can vary a lot by lender, which is why you need to consider closing costs as well as interest rates when shopping for a mortgage.

The amount you can expect to pay in fees will be listed on your Loan Estimate. This is a standard document lenders are required to give you when you apply for a home loan.

The Loan Estimate lets you easily compare fees and understand which lenders are less expensive overall – which may be different from the ones simply offering the lowest mortgage rates.

Comparing closing costs on your loan estimate

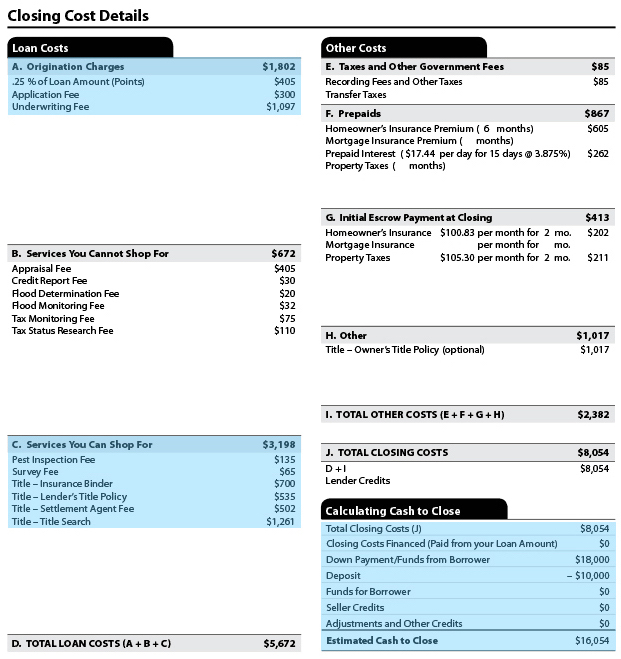

Here’s an example of page 2 of the standard Loan Estimate, which lists all the fees a buyer can expect to pay on closing day.

Image: Consumer Financial Protection Bureau (CFPB)

Pay special attention to section (A), “Loan Costs.” These are the lender’s own fees – which are the main ones you’ll want to look at when comparison shopping.

The first row, “Points,” shows how much you’re paying to buy the rate offered. The next two rows, “Application fee” and “Underwriting fee,” show what lenders charge for their services.

Four ways to avoid closing costs

Home buyers don’t always have to pay closing costs out of pocket.

There are a variety of ways to reduce your costs – or even, if you’re lucky, avoid them altogether.

1. Negotiate closing costs between lenders

Loan Estimates are just offers. And you’re free to negotiate.

If you get some Estimates with lower interest rates but higher closing costs, and vice–versa, call up the lenders and get them to compete for your business.

“I’d love to work with you but your origination fee is X amount higher than lender Y’s,” might be a good start.

Don’t expect your closing costs to go away completely. But you may be able to make a significant dent in your upfront costs or even your interest rate simply by asking.

2. Ask about lender–paid closing costs

Some (but not all) lenders have their own programs that can help with closing costs and down payments. These come in the form of a lender credit.

A lender credit typically means the lender will cover part or all of your upfront costs – and in exchange, you’ll pay a higher interest rate.

For example, Bank of America has its America’s Home Grant® program. It “offers a lender credit of up to $7,500 that can be used towards non–recurring closing costs, like title insurance and recording fees, or to permanently buy down the interest rate [discount points]. The funds do not require repayment.”

And, separately, it provides down payment grants.

As you’d expect, that quote from BoA’s website refers you to a footnote that contains a pile of terms and conditions. But its offer is genuine enough – as are countless others from other lenders.

3. Get the seller to pay your closing costs

Many buyers are able to avoid closing costs by getting the seller to pay them instead.

This arrangement is known as seller concessions.

Typically, the money comes out of the proceeds of the sale. So the seller doesn’t have to cut a check, because the sum is deducted at closing.

Be aware that cash–back is not a possibility here. The total amount of the buyer’s closing costs is the most that can be put on the table.

And, there are limits to the amount of money a seller can contribute to the buyer’s closing costs. By loan type, these limits are:

Conventional loans: 3% of the home’s value with a down payment of less than 10%; 6% with a down payment of 10%–25%; and 9% if bigger

- FHA: 6% of the home’s value

- VA: 4% of the home’s value. But it’s sometimes higher because not all closing costs are counted in calculating your percentage

- USDA: 6% of the home’s value

- Investment properties: 2% of the home’s value

Seller concessions are not uncommon. But the main issue is that sellers are usually only willing to pay the closing costs in a buyer’s market.

However, in a seller’s market – a market with buyer competition – sellers are far less likely to cut such a deal.

In this case, you might want to look elsewhere for help – like a closing cost assistance program.

4. Roll closing costs into your loan amount

Refinance loans have closing costs, just like home purchase loans. And they typically cost around the same amount.

Homeowners looking to refinance can shop around for the lowest closing costs. But there’s no home seller to help them pay.

However, current homeowners have one option home buyers do not: They can often roll closing costs into their loan amount.

Just remember that there’s no such thing as a free lunch.

You’ll be paying down those closing costs – and the interest on them – until you pay down the mortgage, sell the home, or refinance again.

Closing cost assistance

For those who need some extra help with closing costs, there’s one more route to try: closing cost assistance.

Closing cost assistance can come in the form of grants, loans, or gift money to help cover your upfront costs.

Here’s what to know about each one.

Closing cost grants and loans

Closing cost assistance is part and parcel of many down payment assistance (DPA) programs.

There are thousands of down payment assistance programs spread across the country – meaning there’s bound to be one (maybe several) covering the area in which you want to buy.

Each DPA program is different.

- Some offer a loan that you pay back in parallel with your mortgage

- Others provide forgivable loans with no payments that don’t have to be repaid as long as your remain in residence

- Others give outright grants that never have to be repaid

As their name suggests, DPAs primarily exist to help you fund your down payment.

But oftentimes that money can be used to help cover your closing costs, too. Just make sure this is allowed by the program(s) you apply to.

Gift money from family and loved ones

Lenders are generally relaxed about receiving gifts toward your down payment and closing costs from loved ones.

Fannie Mae and Freddie Mac define “loved ones” as family, fiance(e), or domestic partner. But other programs (like FHA loans, for example) widen the field to include close friends.

There are rules about such gifts.

- First, you must provide a letter from the donor confirming that it is an outright gift that never has to be repaid

- Second, you may have to document the source of the funds. For example, if a family member gives you the money and cashes in stocks to do so, they may have to provide a brokerage statement showing his sale of those stocks.

Jon Meyer, The Mortgage Reports loan expert and licensed MLO, says that these rules vary from lender to lender and gift to gift. “With some lenders, when the gift is deposited directly into escrow, we often do not need to source the funds. But if deposited into a borrower’s account first, however, we most likely do.”

This is usually straightforward enough. But lenders can get picky if they suspect that you’re hiding something. So it’s important to make sure your gift funds are correctly sourced and documented.

For more information on how to receive gift funds toward your closing costs, see this article.

Are you ready for the home buying process?

So who pays closing costs? The buyer and seller both do.

If you’re a home buyer, you’ll likely pay 2% to 5% of your loan amount at the closing table (and that’s on top of your down payment).

But if you put in some time comparing lenders and looking for help, you may end up paying a lot less than you would have.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Comments are closed.