Liz Looks at: Stocks vs. Bonds

Six of One, Half Dozen of the Other

“60/40 is dead” has been the recent battle cry of many market pundits after a four decade rally in bonds that was finally ended by the pandemic. This stance is based on the idea that bonds have nowhere to go but down (since rates have nowhere to go but up), and would not offer protection to downside shocks in stocks.

Said another way, the classic “diversified” portfolio consisting of 60% stocks and 40% bonds would not function effectively to protect investors’ downside risk.

This argument made a lot of sense, and I recognize that even with this year’s rise in rates, the absolute level of rates remains at historic lows. But we sit here today with a -8.7% YTD return on 7-10-year Treasury bonds compared to a -6.0% YTD return in the S&P 500. Point being, bonds have sold off a lot, and it’s true they haven’t served as downside protection…yet.

I’m not in the market of calling bottoms, but at some point bonds can enter oversold territory and once again offer upside potential, and a benefit to the traditional stock/bond mix.

Not all Yields Are Created Equal

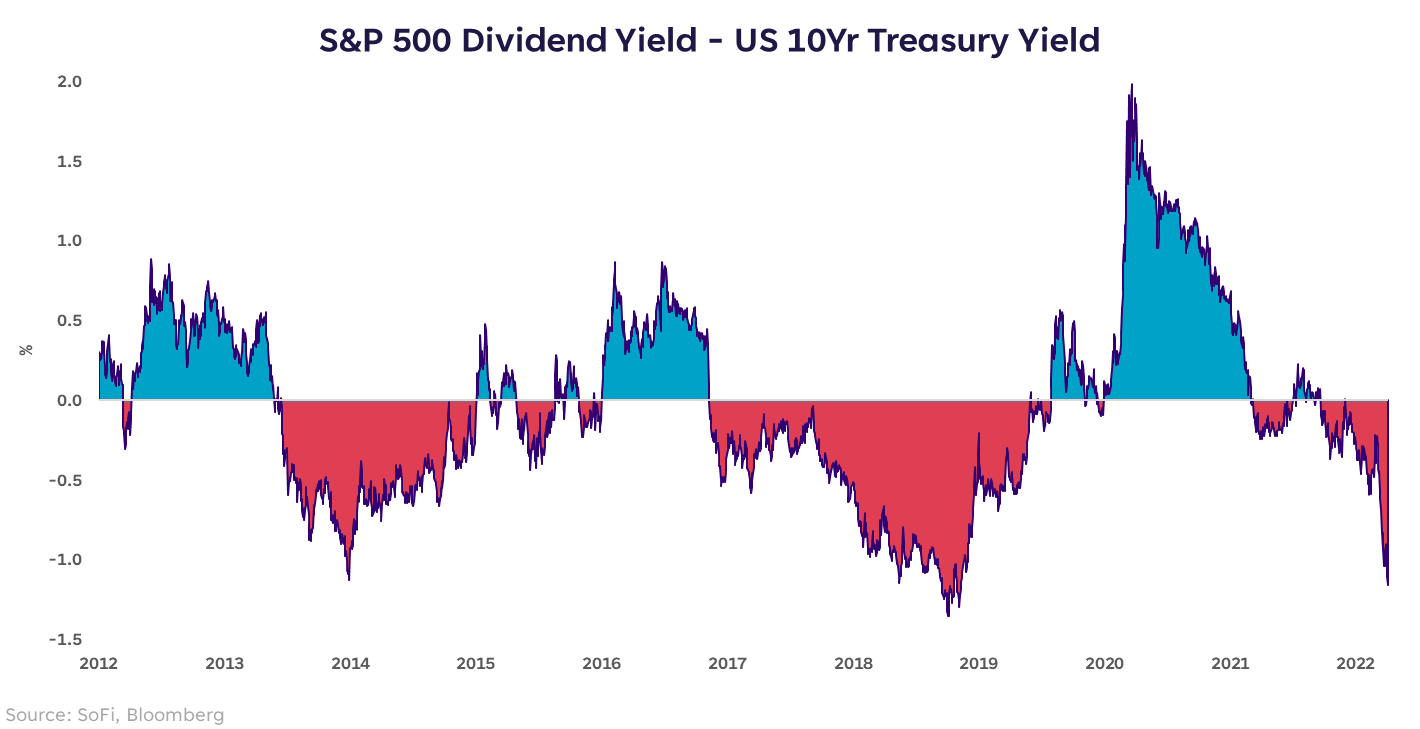

How do we know when that point is? One of the comparisons we can watch is the dividend yield on the S&P 500 vs. the yield on the 10-year Treasury. Yields are a useful metric because they are a function of both the income to be received on a security and the current price of that security.

The simple way to read this chart would be to say the yield on a 10-year Treasury is considerably more attractive than the dividend yield on stocks. But not all yields are created equal. Generally speaking, we buy stocks for their upside potential, not for their dividend income. Whereas bonds are traditionally thought of as an income generating asset. Which means this metric is useful, but not the end-all-be-all decision factor.

Also, in the midst of a tightening cycle and persistently hawkish comments from Fed officials, there is surely more downside possible in bonds (i.e., upside for bond yields). But there’s also more downside possible in stocks. At the current S&P 500 level of ~4,480 and consensus earnings estimates for 2022 of $228/share, that puts the price-to-earnings ratio at 19.6x. That’s still above the 5- and 10-year averages of 18.7x and 17.0x respectively.

The Living Dead?

Back to the 60/40. It may still be dead for a little while, but at some point I’d suggest that Treasury bond yields could hit a ceiling (meaning prices hit a floor) and start moving in the opposite direction. This could be caused by: a breakdown in the economy (thus increasing fear of recession), a moderation in inflation, and/or the Fed turning less hawkish.

None of those things are on the immediate horizon, but they could be on the horizon this year. In which case, 60/40 could rise from the dead.

Want more insights from Liz? The Important Part: Investing With Liz Young, a new podcast from SoFi, takes listeners through today’s top-of-mind themes in investing and breaks them down into digestible and actionable pieces.

Listen & Subscribe

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

SOSS22040702

Comments are closed.