Liz Looks at: July Inflation

Running of the Bulls

Bullish sentiment was the star of the show yesterday as year-over-year July CPI came in at 8.5% — below estimates and below June’s hottest read of the cycle yet at 9.1%. More importantly perhaps, the month-over-month reading was 0.0%, indicating no movement upward at all (on headline CPI). Even the core CPI data surprised to the downside for July.

The obligatory hedging statement is: this is only one month of cooling and one month does not make a trend. We need to see this for at least three consecutive months before the Fed feels satisfied enough to take a less aggressive stance. But, we have to start somewhere, and this is a decent start.

Uno, Dos, About Face

Markets were waiting for a reason to justify the recent rally, and at least some encouragement that the “peak inflation” calls were correct in June. With both of those boxes ticked yesterday, the rally that ensued was a powerful one with the S&P up 2.1% and Nasdaq rising 2.9% to clock in a 20.8% rise from its recent low on June 16th.

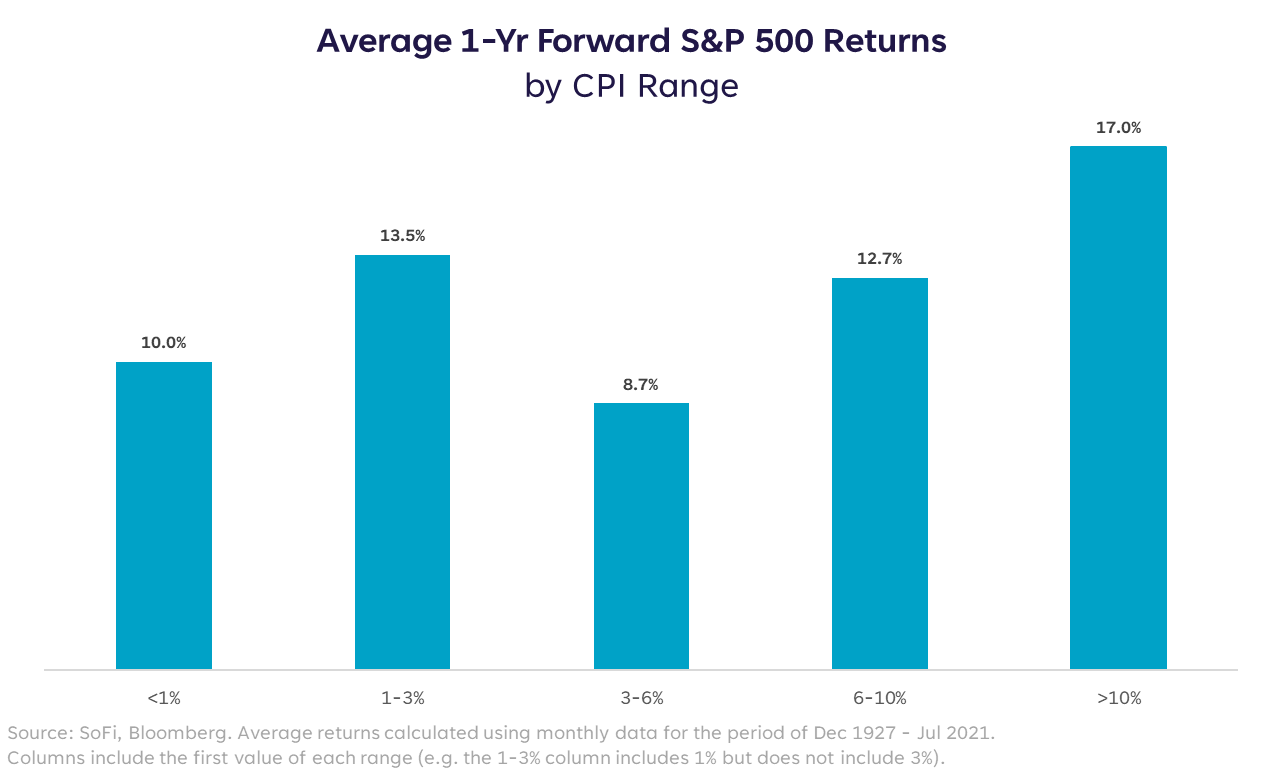

We can’t decidedly declare victory with inflation still at 8.5%, but we can look at prior inflation regimes and see how the market did during each to try to understand the risk/reward as investors. The chart below shows different ranges of headline CPI data and the corresponding average forward 12-month return on the S&P 500.

I’ve long believed that there was such a thing as an inflation “sweet spot” between 1-3%, where the market could generally rise without much worry about whether the economy was too hot or too cold. This creates more flexibility around the Fed’s 2% target and removes the labels of “good” or “bad” from anything that isn’t exactly 2%.

The data largely agrees with that theory, with the 1-3% bucket exhibiting higher average returns than every other bucket except the >10% range. But let’s be clear…that >10% bucket is an extreme environment that typically doesn’t last long, and has a host of other consequences that I’d prefer to live without. Also, only 6% of the 1,124 observations fall into that range.

The only problem here is that we’ve got a long way to go before we reach the top end of that range and hit 3% on headline CPI.

Quizás, Quizás, Quizás

Although I was, and still remain, somewhat skeptical of the swift rise we’ve seen in markets since mid-June because it feels more like risk-on multiple expansion (i.e., not fundamentally driven), I standby my statement that investors should be in the market and out of cash before the end of summer.

In Spanish, the word “suave” translates to “soft.” Rarely do we wish for softness in markets, but in the case of the Fed’s current goal, markets are starting to believe in the possibility of a soft landing. If we call it a “suave landing” it sounds more like a game of skill than a happy accident. No one truly knows what’s going to happen, but I believe that the remainder of 2022 can be characterized in markets as a period of “suave landing” upside.

That said, if you’re familiar with the actual Running of the Bulls that takes place in Pamplona, Spain each summer, you know it’s far from a peaceful jog through the city. We’re still being chased by the angry animal that is inflation, and our heart rate is still elevated, but the race is underway. And the further we get without meaningful injury, the more likely a successful finish becomes.

Want more insights from Liz? The Important Part: Investing With Liz Young, a new podcast from SoFi, takes listeners through today’s top-of-mind themes in investing and breaks them down into digestible and actionable pieces.

Listen & Subscribe

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

SOSS22081101

Comments are closed.